The $270 Billion Race to Replace the Panama Canal

The Panama Canal stands as one of the most powerful arteries of global trade. I have watched its story shift from mechanical triumph to climate vulnerability in real time. You rely on this narrow waterway every day, even if you never see it. About five percent of all global maritime cargo still flows through its locks, moving food, fuel, consumer goods, and raw materials between two oceans. The canal channels roughly $270 billion in trade value each year and delivers almost $5 billion in direct annual revenue to Panama. Yet in 2024, the world confronted a reality once considered impossible. The canal ran out of water. I followed the unfolding crisis ship by ship, watching lines of vessels stretch across the Pacific entrance while rates surged across global supply chains as though a fuse had snapped beneath world commerce.

At the peak of the drought in early and mid-2024, transit capacity collapsed from the typical 36 to 38 ship passages per day to about 24. Some vessels waited weeks for slots. Freight rates on Asia to East Coast North America routes multiplied by as much as four in short spikes. Cargo owners rerouted through the Suez Canal or sent ships around Cape Horn, restoring a thousand-mile detour once erased by Panama’s opening. From that moment forward, nations across the Americas recognized an opening that may never come again. I stood in logistics hubs feeling the urgency firsthand. If the Panama Canal could no longer guarantee reliability, someone else would attempt to replace or bypass it.

The Legacy the World Still Depends On

When the Panama Canal opened in 1914, it reshaped global geography overnight. Before the canal, every ship traveling between the Atlantic and Pacific Oceans spent weeks navigating the southern tip of South America. The canal sliced through the Isthmus of Panama and erased nearly 12,000 kilometers from typical shipping routes. Construction between 1904 and 1914 became one of history’s most difficult engineering campaigns. Crews moved more than 200 million cubic meters of earth through swamps and mountains. Engineers battled malaria, yellow fever, landslides, and torrential rain. Labour losses reached close to 6,000 lives. The build cost $375 million at the time, equal to more than $22 billion in modern value.

That sacrifice created more than a shortcut. The canal became strategic infrastructure linking continents, naval routes, energy exports, food supply chains, and manufacturing corridors. It remains central to Panama’s national economy and international relevance. In fiscal year 2024, the Panama Canal Authority reported $4.99 billion in revenue and $3.45 billion in net profit, reflecting sustained demand even under crisis conditions.

Also Read: China’s $10 Billion Mega Canal Project: The Next Panama Canal?

The Water Crisis That Changed Everything

Gatun Lake supplies freshwater to the canal’s locks. Each transit empties millions of gallons into the sea. The canal lives or dies by seasonal rainfall feeding this reservoir. In 2024, an El Niño-driven drought crushed water levels to the lowest point in six decades. Operators restricted vessel draft limits to prevent groundings and reduced daily passages to preserve supplies. Large container ships sailed under-loaded. Bulk carriers cut capacity. LNG shipments delayed transfers to Europe and Asia. Supply networks built on just-in-time shipping fractured.

By mid-2025, heavier rainfall restored partial stability. Current daily transit rates recovered to roughly 31 or 32 vessels per day. Draft limits remain active. Long term risk remains unresolved. Climate models supported by NOAA and the World Meteorological Organization predict longer dry seasons across Central America, reducing freshwater inflows that the canal depends on. The emergency never truly faded. It simply stabilized.

For shipping markets, the canal’s vulnerability triggered structural reassessment. You can feel that shift across port expansions, rail corridors, and revived mega canal studies. Regional governments now see a chance to challenge Panama’s monopoly position for the first time since 1914.

Why New Routes Now Make Sense

With over $270 billion in goods moving annually through the canal, even a partial diversion creates enormous opportunity. Delays and unpredictability now cost shipping lines millions per month. Ports compete fiercely for transshipment volumes. Logistics sovereign strategies take shape across Latin America. The race focuses on speed to deployment rather than sheer ambition.

Countries discovered a blunt truth. Building a parallel canal requires decades and magnitudes of funding. Rail landbridges offer faster alternatives at billions rather than tens of billions. You see this strategic divergence emerging clearly across the region.

Mexico’s Interoceanic Corridor

Mexico currently leads the race through execution rather than spectacle. Its Interoceanic Corridor of the Isthmus of Tehuantepec links Coatzacoalcos on the Gulf of Mexico with Salina Cruz on the Pacific. The corridor centers on a 308 kilometer freight railway connecting port terminals supported by new container yards and customs processing zones.

Investment stands around $7.5 billion. Trial cargo movements began operating in late 2024. Mexico targets scaling to 1.4 million containers annually by 2033, which remains modest against Panama’s annual throughput above 14 million TEUs but still significant for overflow and time-critical shipments.

The transloading requirement introduces inefficiencies. Containers must unload, transfer to rail, then reload at the opposite port. That process adds handling costs. Yet compared to multi-week waiting periods at Panama, the corridor offers an emergency pressure valve that many shipping lines now treat as a viable contingency route. I have observed shipping companies quietly routing pilot volumes through the corridor to assess reliability and insurance risks.

Colombia’s Atlantic Pacific Rail Vision

Colombia seeks to replicate the landbridge idea with a 240 kilometer railway connecting Cupica on the Pacific coast to the Caribbean near Turbo. Cost projections range from $7 billion to $13 billion, depending on tunnels, elevation alignment, and port dredging needs. The scheme integrates into Colombia’s national plan to reactivate more than 1,800 kilometers of freight rail to reposition the country as a logistics hub.

Challenges remain severe. Routing penetrates biodiverse rainforest zones and recognized indigenous territories, triggering lengthy environmental approvals. Engineering complexities include mountainous grades and landslide risk. As of 2025, the project remains in feasibility review with no construction awarded. Political consistency and investor confidence remain uncertain.

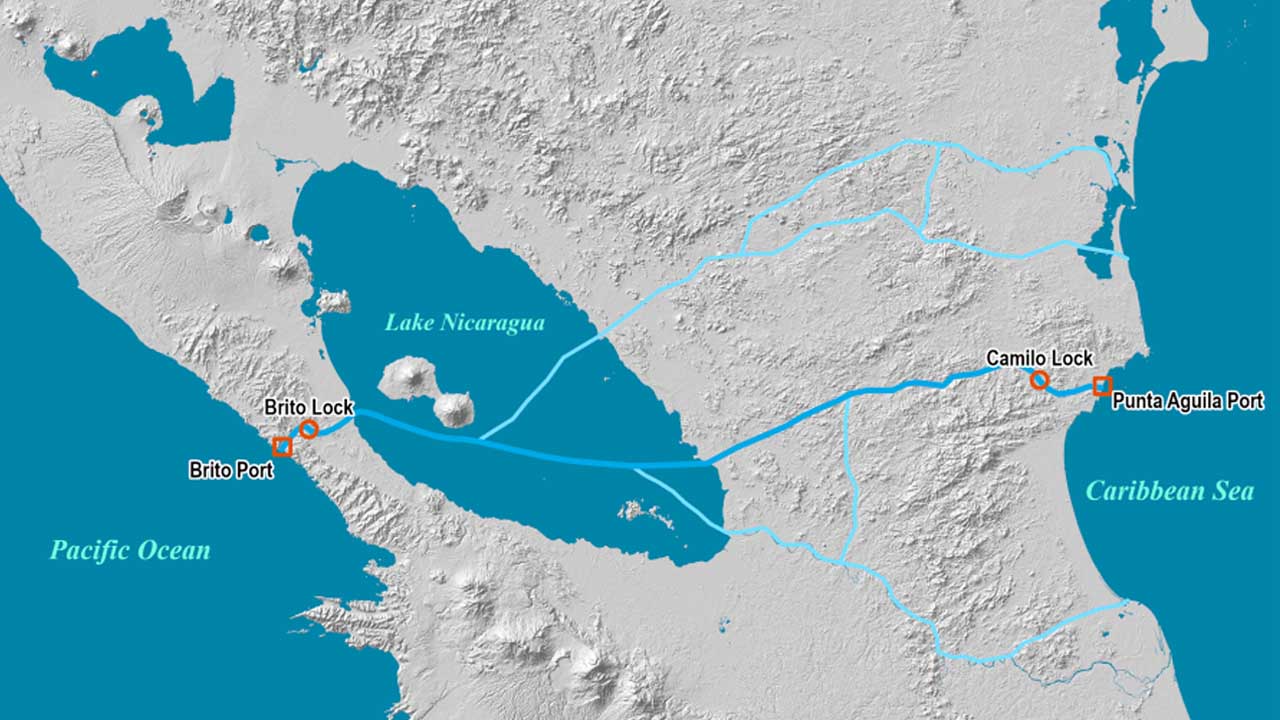

Nicaragua’s Unfinished Mega Canal

No proposal ever matched the scale of Nicaragua’s interoceanic canal dream. Planners envisioned a 278 kilometer canal with lock chambers larger than Panama’s Neopanamax system. Lock dimensions stretched to 510 meters long, 77 meters wide, and 27 meters deep, capable of passing ultra-large container ships without size restrictions.

The estimated price tag reached $64.5 billion. Chinese financier Wang Jing initially backed the scheme with government concessions signed in 2013. Funding evaporated in 2018. Environmental opposition intensified over the canal’s proposed path through Lake Nicaragua, Central America’s primary freshwater source. Community displacement and ecosystem damage raised international condemnation. No credible replacement funding emerged. Only early survey works and access roads remain visible. As of 2025, the project sits dormant without financial revival.

Secondary Players and Northern Routes

Honduras promotes its own bi-oceanic rail link connecting Amapala on the Pacific to Puerto Castilla on the Caribbean, backed by Chinese engineering discussions since 2023. No binding financing has materialized.

Panama itself studies container landbridge systems using upgraded rail corridors parallel to the canal, aiming for transshipment capacities approaching five million TEUs annually by 2045.

Far north, Arctic sea ice retreat slowly reveals the Northwest Passage. Marine insurers treat the route as seasonal risk exposure due to drifting ice and absent emergency infrastructure. Commercial deployment remains extremely limited.

Panama’s Counteroffensive

Panama understands the stakes. The canal authority authorized a $1.6 billion dam project on the Indio River basin to feed Gatun Lake. Completion targets 2030 to 2031. The dam increases reservoir capacity sufficiently to sustain approximately 36 daily vessel transits even during prolonged drought cycles.

Canal operations tightened booking rules to one daily slot per operator to reduce auction inflation and ensure equal distribution. The newer lock complexes operate at around seven percent lower freshwater use per transit through basin recycling systems, conserving millions of cubic meters annually.

Despite the crisis, Panama retains a structural advantage. Rail landbridges shift containers but cannot match the uninterrupted transit speed of a continuous waterway once constraints ease. Shippers prefer single-ship crossings when capacity allows. Panama’s active investments aim to preserve that advantage.

The Battle’s Financial Reality

Mexico invests $7.5 billion for 1.4 million TEUs per year capacity. Colombia estimates up to $13 billion for a route still on the drawing board. Nicaragua requires over $64 billion without funding. Panama protects its dominance with a $1.6 billion water stabilization project that sustains full-scale operations.

The rivalry reveals the biggest truth. Full canal replacement remains impractical. Diversion corridors function as supplements rather than substitutes. The real contest separates resilience from vulnerability rather than replacement from obsolescence.

Also Read: Inside the $20 Billion Eurasia Canal That Could Rewrite Global Trade

The Future of the World’s Shortcut

The Panama Canal once represented certainty. Climate volatility removed that certainty and forced redundancy into global shipping plans. I see this evolution firsthand across port infrastructure bids and rail concession talks. You now live in a world where shipping route diversification shapes trade strategy as much as vessel size or port efficiency.

Mexico’s corridor will absorb overflow traffic during future droughts. Colombia may follow if financing stabilizes. Nicaragua’s dream could revive under new geopolitical backers but faces insurmountable environmental and social barriers.

Yet Panama retains the crown. Active engineering adaptation, localized water solutions, and decades of operational mastery keep it unmatched. The canal no longer stands alone, but it remains irreplaceable.

From the lock walls overlooking Gatun Lake, watching container ships inch forward under tight draft limits during the height of the crisis gave me a clarity no data chart can convey. The canal will survive this era not through ambition, but through relentless adaptation shaped by necessity.